Real-World Asset Tokenisation

Everything can become a Token

Jamie Shipley

11/18/202522 min read

Real-World Asset (RWA) tokenization represents one of the most transformative innovations in blockchain technology and finance today. By converting physical and traditional financial assets into digital tokens on distributed ledgers, tokenization is fundamentally reshaping how assets are owned, traded, and managed globally. The market has experienced explosive growth, expanding from $2.9 billion in 2022 to over $612 billion in 2025, with projections suggesting the industry could reach $9.43 trillion by 2030. This acceleration reflects a critical convergence: blockchain technology has matured sufficiently to handle institutional-grade financial products, regulatory frameworks are beginning to provide clarity, and institutional participants—including BlackRock, Franklin Templeton, and major banks—are actively deploying tokenized assets. For businesses and investors, this shift is no longer theoretical; it represents an immediate opportunity to participate in a more efficient, transparent, and accessible global financial system. This article explores the mechanisms, benefits, real-world applications, and transformative potential of RWA tokenization, offering insights for those seeking to understand and engage with this emerging financial infrastructure. Understanding Real-World Asset Tokenization: Definition and Fundamentals

Real-World Asset tokenization is the process of converting tangible or traditional financial assets into digital tokens on a blockchain network. Unlike cryptocurrencies, which exist purely as digital entities, or non-fungible tokens (NFTs), which represent unique digital items, RWA tokens derive their intrinsic value from underlying physical or financial assets such as real estate, bonds, commodities, stocks, or intellectual property rights. Each token represents a claim on either full or fractional ownership of the corresponding asset, with the ownership rights and economic benefits embedded into the token's smart contract logic.

The fundamental innovation of tokenization lies in its ability to fractionalise traditionally illiquid assets. Previously, purchasing a luxury commercial property or investing in a multi-million-dollar real estate portfolio required substantial capital and access to specialized investment channels. Tokenization democratizes this access: a single commercial building can be divided into thousands of tradeable tokens, enabling retail investors to own fractional stakes while allowing global capital pools to participate in previously restricted markets.

The blockchain infrastructure supporting RWA tokenization provides several critical advantages over traditional systems. Unlike centralized databases maintained by financial institutions, blockchain creates an immutable, transparent ledger where all transactions and ownership records are permanently recorded and verifiable by all network participants. This transparency dramatically reduces fraud risks, improves audit capabilities, and enables continuous settlement—meaning transactions can be finalized in seconds rather than the days or weeks required by legacy financial systems. The integration of smart contracts automates complex processes, from dividend distribution to compliance checks, eliminating intermediaries and reducing operational friction.

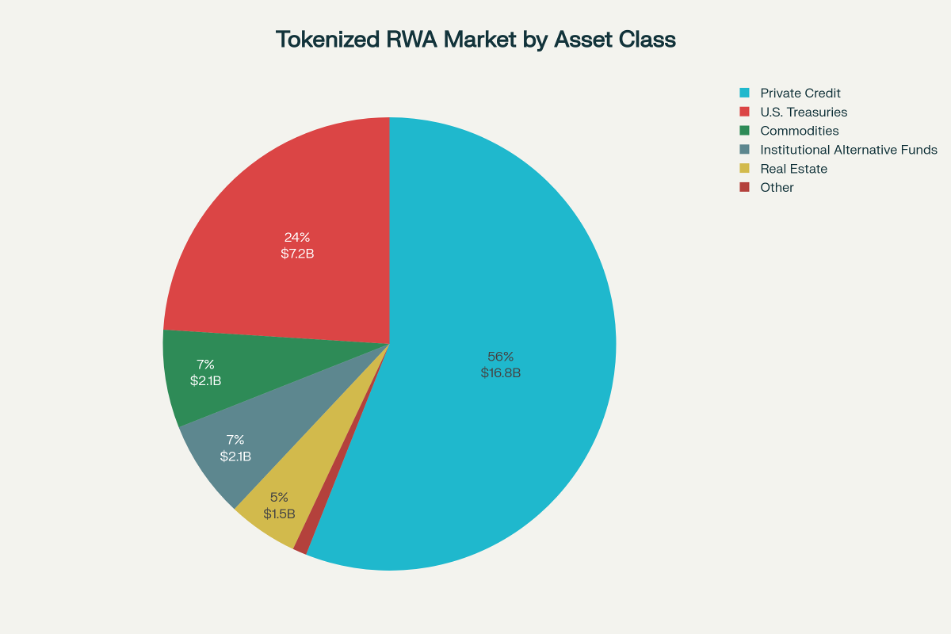

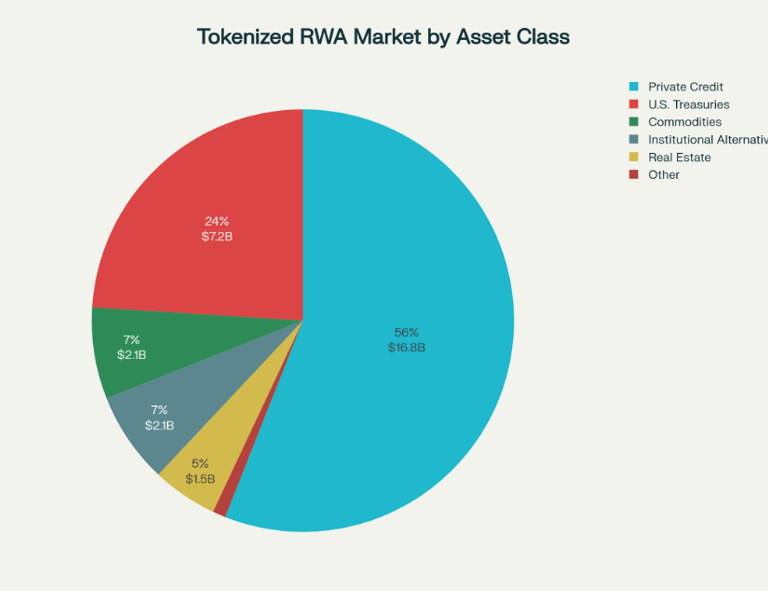

The total value locked in tokenized RWAs reached approximately $30 billion by Q3 2025, demonstrating real institutional adoption and investor appetite. This represents genuine capital flows into blockchain-based financial systems, not speculative trading. The largest segments—private credit ($16.8 billion) and U.S. Treasuries ($7.2 billion)—are precisely the asset classes that traditional financial institutions rely upon, signifying that tokenization has moved beyond niche experimentation into mainstream financial practice.

RWA Tokenization Market Growth: Historical Performance and 2030 Forecast

Strategic Benefits of Tokenization: Why This Technology Matters

The adoption of RWA tokenization is driven by tangible, measurable benefits that appeal to both institutional and retail investors, as well as asset issuers and custodians. Understanding these advantages explains why major financial institutions are investing heavily in tokenization infrastructure and why regulatory bodies are rushing to establish frameworks to accommodate this technology.

Enhanced Liquidity and Market Access

One of the most compelling benefits of tokenization is the dramatic improvement in asset liquidity. Traditional real estate, private equity, and corporate debt are notoriously illiquid—once an investor commits capital to these assets, they may face extended lock-up periods or face significant penalties for early exit. Tokenization enables continuous, 24/7 trading on digital exchanges, breaking the constraints of traditional market hours and geographic barriers. A property tokenized in Dubai can be traded to an investor in Singapore, and settlement can occur within minutes rather than the weeks required to process traditional international transfers.

This enhanced liquidity has profound economic implications. For investors, it means capital that was previously trapped in illiquid assets can be redeployed more quickly to capitalize on new opportunities. For issuers, improved liquidity attracts broader investor pools, enabling asset owners to raise capital more efficiently. McKinsey estimates that improved liquidity conditions alone could unlock trillions of dollars in previously inaccessible capital markets.

Fractional Ownership and Democratized Access

Tokenization fundamentally changes the barrier to entry for high-value assets. Consider traditional real estate investment: purchasing a commercial property typically requires capital ranging from hundreds of thousands to millions of dollars, restricting participation to wealthy individuals and institutional investors. By tokenizing that property, the same investment can be fractionalised into thousands of tokens, each representing a proportional share of the asset's ownership and income streams. A retail investor with $5,000 to deploy can now own a stake in a portfolio of premium properties globally, an opportunity previously unavailable to them.

This democratization extends beyond real estate. Tokenized U.S. Treasury bonds through platforms like Ondo Finance now enable individual investors to purchase fractions of government debt instruments that traditionally required minimum investments of $10,000 to $1 million. Art collectors can own fractional stakes in masterpieces; private equity investors can participate in venture funds with lower minimums; commodity traders can diversify across precious metals and crude oil with smaller capital allocations. This accessibility transformation is reshaping capital markets architecture by enabling a significantly broader population to build diversified, yield-generating portfolios.

Reduced Transaction Costs and Operational Efficiency

Traditional financial infrastructure is expensive. Processing an international real estate purchase involves multiple intermediaries—lawyers, brokers, custodians, clearing houses, settlement agents—each extracting fees. A typical commercial real estate transaction incurs legal costs of 1-3% of the asset value, broker commissions of 5-6%, transfer taxes, and ongoing custodial fees averaging 0.5-1% annually. Smart contract automation and blockchain settlement can reduce these costs by up to 30 percent, according to industry studies.

The operational impact is equally significant. Traditional settlement for securities takes 2 business days (T+2); cross-border transfers can require weeks as correspondent banks route transactions through multiple intermediaries. Blockchain-based settlement is instantaneous, with tokens transferring in seconds once all conditions are met. This efficiency gain accelerates capital flow, reduces counterparty risk (since assets settle atomically rather than through multiple sequential steps), and frees compliance teams to focus on higher-value activities rather than manual transaction processing.

Enhanced Transparency and Reduced Fraud Risk

Every token transaction is recorded on an immutable blockchain ledger, creating permanent, auditable records that regulatory authorities and investors can access in real-time. This transparency eliminates numerous fraud vectors that plague traditional finance. In real estate, tokenization prevents double-selling through cryptographic proofs of ownership. In securities trading, it eliminates settlement failures and reduces naked short-selling. In commodity markets, it enables authentic supply chain verification and prevents fraud in provenance claims.

For institutional investors, this transparency translates to reduced due diligence costs and faster investment decisions. Traditional real estate investment funds require extensive on-site audits; tokenized properties can provide verifiable, real-time asset valuations through automated data feeds. This capability is particularly valuable in emerging markets with less transparent legal systems, where blockchain-based records can provide stronger assurances than local documentation.

Superior Compliance and Programmable Regulations

Smart contracts encode compliance rules directly into token transfers. When an investor attempts to transfer a security token, the smart contract automatically verifies that the buyer is properly accredited, that their identity has passed KYC/AML checks, and that the transfer complies with regulatory restrictions on security transfers. This programmability shifts compliance from a reactive, post-transaction audit function to a proactive, built-into-the-transaction enforcement mechanism.

The result is that regulatory compliance becomes faster, more consistent, and less prone to human error. What previously required a compliance officer to manually review transactions now occurs automatically through code. This is particularly important in cross-border transactions, where multiple regulatory jurisdictions apply; smart contracts can encode the complex rules from each jurisdiction and automatically enforce them without requiring manual intervention.

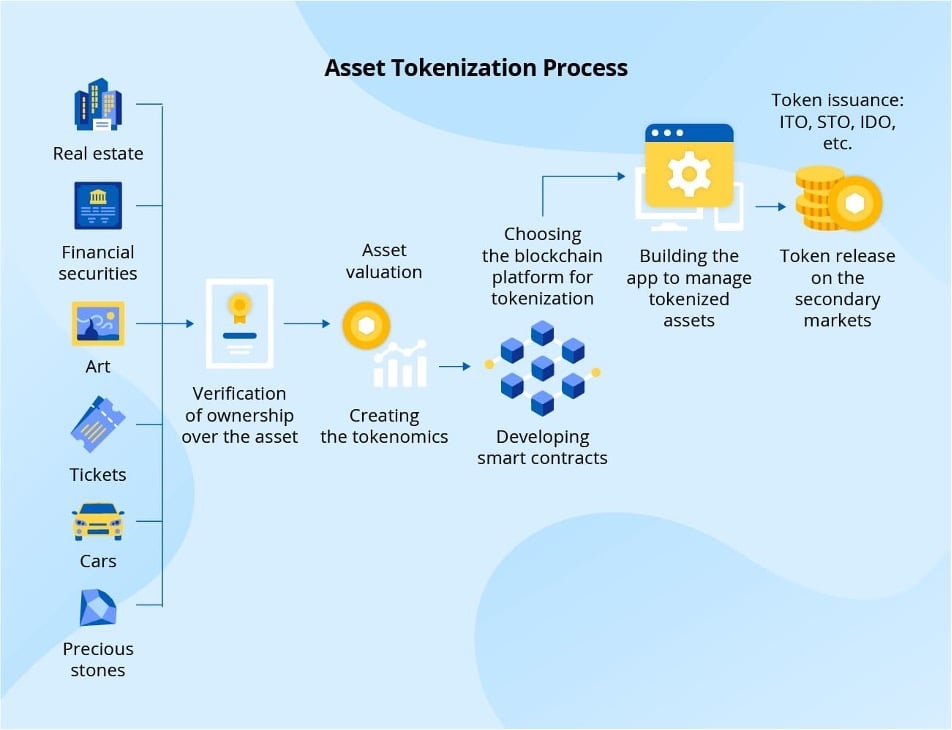

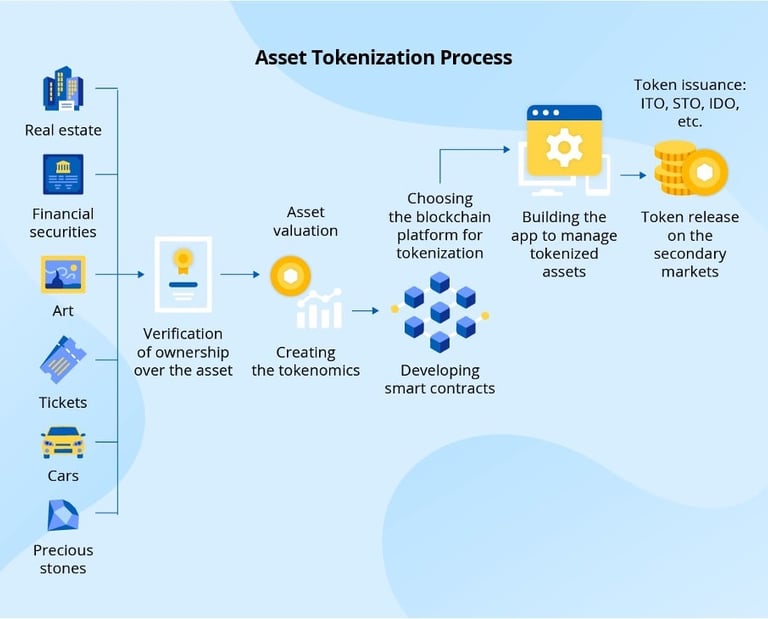

The Tokenization Process: How Real-World Assets Move On-Chain

Understanding the technical and operational process of tokenizing assets is essential for grasping how legitimate, compliant RWA tokenization differs from fraudulent schemes. The process involves multiple sequential stages, each requiring specific expertise and carrying distinct risks.

Step 1: Asset Selection and Evaluation

Tokenization begins with selecting a suitable asset and conducting thorough due diligence. The asset must be valuable, identifiable, and capable of generating returns or holding stable value. Real estate is valuable and identifiable but requires physical inspection and market valuation. Securities are easily valued but must be verified as legitimate and unencumbered. Commodities can be verified through commodity exchanges but may face price volatility challenges. The evaluation process includes legal verification of title, assessment of liens or encumbrances, valuation using market-standard methodologies, and identification of any legal impediments to tokenization.

This initial stage is where many tokenization projects fail or face challenges. An asset with unclear legal title, disputed ownership, or regulatory restrictions cannot be successfully tokenized. Leading platforms like BlackRock BUIDL , Ondo Finance, and Securitize invest heavily in this stage, conducting extensive legal research and due diligence to ensure that the assets they tokenize have clear, enforceable claims against them.

Step 2: Legal Structuring and Special Purpose Vehicles

For most RWA tokenization projects, the asset is placed into a Special Purpose Vehicle (SPV), a legal entity created specifically to own and manage that asset. The SPV structure serves multiple purposes: it isolates the asset from the issuer's bankruptcy risk, provides a clear legal container for the asset that holders have claims against, and enables the tokens to represent fractional ownership stakes in the SPV rather than direct ownership of the asset itself.

This legal structuring must comply with jurisdiction-specific regulations. In the United States, SPVs are typically structured as limited liability companies or limited partnerships under state law. In Europe, particularly under MiCA (Markets in Crypto-Assets Regulation), additional requirements apply around how token rights attach to the underlying assets. The legal documentation must clearly specify what rights each token grants to its holder—whether they include dividend rights, voting rights in the SPV, rights to asset liquidation proceeds, or combinations thereof.

MakerDAO's approach to RWA integration illustrates the sophistication of these legal structures. For capturing value from off-chain assets while maintaining decentralized governance, MakerDAO established a foundation and SPVs to hold underlying assets, with community voting controlling these legal entities' key decisions while smart contracts enforce the agreed terms on-chain. This hybrid legal-technical structure has enabled MakerDAO to access billions of dollars in real-world asset value while maintaining its core decentralized governance principles.

Step 3: Token Specifications and Blockchain Selection

Once the legal structure is established, the team must define the token's technical specifications: Will it be a fungible ERC-20 token (where each token is identical and interchangeable) or a non-fungible ERC-721 token (where each token represents a unique asset)? Will it be divisible into decimals, or represent whole units only? What blockchain network will it exist on—Ethereum for maximum ecosystem integration, Polygon for lower costs, Solana for throughput, or an alternative chain?

The blockchain selection decision involves trade-offs. Ethereum offers the largest ecosystem of compatible DeFi applications and institutional custody solutions but carries higher transaction fees. Polygon and other Layer-2 solutions reduce fees to near-zero levels but may have smaller investor bases. Some issuers deploy tokens across multiple blockchains simultaneously to maximize liquidity and investor access. Ripple's partnership with Ondo Finance, for example, brings tokenized U.S. Treasuries to the XRP Ledger while maintaining parallel deployments on Ethereum, providing investors with choice in which blockchain to execute transactions on.

Step 4: Token Minting and Custody Arrangement

With technical specifications finalized, the actual tokens are minted (created) on the blockchain and recording mechanisms established. Simultaneously, custody arrangements must be finalized. This is a critical risk management step: the underlying asset must be held in custody by a qualified, regulated custodian—either an institutional-grade third-party custodian like Fireblocks or BitGo (for crypto-native tokens) or a traditional financial custodian (for traditional securities or real estate).

The custody arrangement must be verified through periodic "Proof of Reserve" mechanisms, ensuring that the assets backing the tokens actually exist and are properly safeguarded. Chainlink's Proof of Reserve services, for example, provide periodic on-chain attestations that verify custody of backing assets, enabling token holders and DeFi protocols to confirm that collateral is properly held.

Step 5: Investor Onboarding and KYC/AML Compliance

Before tokens can be offered to investors, all prospective buyers must pass Know Your Customer (KYC) and Anti-Money Laundering (AML) checks. This process involves identity verification, source-of-funds verification, and sanctions screening. Modern platforms integrate KYC/AML into their user interfaces, enabling investors to complete verification within minutes rather than the days or weeks traditional banks require.

This compliance step is essential because most tokenized RWAs are regulated as securities in their home jurisdictions. Securities regulations restrict who can purchase them; accredited investors can access broader offerings than retail investors. Smart contracts are programmed with these restrictions, automatically preventing unauthorized transfers and enforcing investor qualification requirements.

Step 6 and 7: Primary Offering and Secondary Trading

Once investor qualification is complete, tokens are offered on primary marketplaces (the initial issuance), and subsequently trade on secondary markets. The primary offering enables capital raising; the secondary market provides liquidity for existing token holders seeking to sell their stakes.

Leading secondary trading venues include regulated digital asset exchanges (like Coinbase or Kraken, which are expanding into tokenized asset trading), specialized RWA trading platforms (like RealT for real estate or tZERO for securities), and DeFi protocols (like Aave, which is integrating RWA tokens as collateral into its lending platform). The presence of robust secondary trading venues is critical to investor confidence; without assured liquidity, many investors will decline to commit capital.

Step 8: Ongoing Management and Revaluation

Tokenized assets require continuous management: real estate generates rental income that must be distributed to token holders; bonds pay interest; equities may generate dividends; commodity positions must be monitored for price movements. Asset issuers must maintain compliance, conduct periodic revaluations to ensure tokens remain fairly priced, and manage investor communications.

Smart contracts automate many of these management tasks. Revenue distributions can be automatically triggered and distributed to token holders based on smart contract logic. Compliance checks can be continuously executed, automatically restricting trading if necessary. Revaluation oracle feeds can be integrated to maintain accurate token pricing. However, some management functions—particularly decisions about asset selling, refinancing, or major operational changes—typically require governance mechanisms that involve token holders or appointed boards making decisions through formal processes.

Infographic showing the detailed process of asset tokenization from verifying ownership to token release on secondary markets.

Leading Use Cases: Tokenization Reshaping Financial Markets

The practical applications of RWA tokenization extend across numerous asset classes, each with distinct benefits and implementation challenges. Understanding these use cases illustrates the breadth of tokenization's potential impact.

Real Estate Tokenization: Democratizing Property Investment

Real estate tokenization is arguably the most mature use case, with over $20 billion in tokenized real estate globally and projections suggesting the market could grow to $1.5 trillion by 2030. The real estate sector benefits particularly from tokenization because property is heterogeneous (each building is unique), illiquid (traditional sales take months), capital-intensive (purchases require substantial capital), and generates clear income streams (rental revenue).

Practical examples demonstrate the technology's real-world viability. The St. Regis Aspen Resort, tokenized by SolidBlock in 2022, raised $18 million by offering fractional ownership stakes in the luxury hotel, demonstrating that hospitality investors will accept blockchain-based ownership of premium properties. RealT has tokenized hundreds of rental properties, primarily in U.S. cities like Detroit, Chicago, and Atlanta, enabling investors to own fractional stakes in individual homes and receive daily rental income payouts in stablecoins. The Brickblock project tokenized Berlin apartment complexes, opening access to European real estate for global investors while providing transparent rental return tracking.

In Dubai, multiple platforms including Qarat and XRP Dubai have launched real estate tokenization initiatives that leverage the UAE's progressive stance toward blockchain innovation. These projects enable international investors to purchase digital shares in commercial properties, retail centers, and residential developments, all while complying with local regulations. The ability to tokenize real estate in one of the world's most sought-after property markets demonstrates that premium assets now have blockchain-based alternatives to traditional ownership structures.

The benefits for real estate are compelling: developers gain access to global capital pools faster and cheaper than traditional financing; investors gain fractional access to portfolios they could never afford individually; token holders receive transparent, real-time accounting of rental revenue and property valuations; and smart contracts automate rental collection, maintenance fund accumulations, and tax documentation.

Tokenized Treasury Securities and Government Bonds

Institutional adoption of RWA tokenization accelerated when major financial institutions began tokenizing government securities. This use case addresses a fundamental problem in traditional finance: treasury bond markets are enormous ($25+ trillion globally) but access is fragmented, expensive to operate, and limited by market hours. Tokenizing treasuries into 24/7, instantly tradeable digital assets unlocks significant efficiency.

Ondo Finance has become a leader in this space, accumulating over $1.3 billion in total value locked, with its OUSG (Ondo Short-Term U.S. Government Securities) token exceeding $690 million in assets under management. OUSG tokens are backed by the BlackRock USD Institutional Digital Liquidity Fund (BUIDL), meaning investors gain exposure to short-term treasuries through a blockchain-native token that can be traded 24/7 with instant settlement.

The Ripple and Ondo Finance partnership brought OUSG tokens to the XRP Ledger in 2025, enabling institutional investors to execute treasury transactions on XRPL using Ripple's RLUSD stablecoin. This arrangement provides low-latency, instant settlement compared to traditional T+2 settlement, dramatically reducing counterparty risk and operational complexity.

Franklin Templeton, one of the world's largest fund managers, has also embraced RWA tokenization, launching tokenized money-market funds that enable institutional investors to access high-quality liquid assets through blockchain infrastructure. Goldman Sachs and BNY Mellon have partnered with multiple platforms to tokenize money-market funds, further validating institutional adoption.

The regulatory significance of treasury tokenization cannot be overstated. Treasuries are the safest financial instruments; if blockchain technology can securely tokenize government debt while maintaining regulatory compliance, it demonstrates that the technology is suitable for the broadest possible range of financial assets.

Private Credit and Fixed Income Tokenization

Private credit markets represent another frontier for RWA tokenization. Private loans, corporate debt, and structured credit products are estimated at $1.2+ trillion globally but remain predominantly held by institutional investors due to high minimum investment requirements, limited liquidity, and illiquidity-driven illiquidity premiums that make these investments expensive to access.

Tokenization addresses these challenges by enabling fractional participation in private credit portfolios. MakerDAO's integration of private credit through platforms like Centrifuge and partnerships with firms like BlockTower Credit demonstrates how decentralized protocols can access institutional credit markets. MakerDAO's DAI stablecoin is partially backed by tokenized private credit, providing yield for DAI holders while enabling small investors to participate in credit markets that traditionally required $5 million+ minimums.

As of Q3 2025, private credit represents the largest segment of tokenized RWAs at approximately $17 billion, demonstrating substantial investor appetite for these products. The advantage for borrowers is profound: they gain access to global pools of capital willing to hold fractional stakes in their debt, potentially lowering borrowing costs. For investors, they gain exposure to yield premium above treasuries through diversified credit portfolios accessible to retail participants.

Carbon Credits and Environmental Commodity Tokenization

Carbon credit markets are projected to reach $1.6 trillion by 2028, growing at 31% annually. Tokenization is transforming these markets by creating verifiable, tradeable digital records of carbon offsets. Toucan, a carbon credit bridging protocol, converts traditional carbon credits into ERC-20 tokens (TCO2) that can be traded on decentralized exchanges and integrated into DeFi protocols.

This application illustrates tokenization's potential beyond financial assets. Environmental commodities are exactly the type of asset that benefit from tokenization: their value is abstract (tons of carbon dioxide reduced or avoided), enforcement must be transparent and globally verifiable, markets are fragmented, and retail participation has been minimal. By tokenizing carbon credits, these projects democratize green investment access while creating transparent, auditable records of environmental impact.

Intellectual Property and Patent Rights

Intellectual property represents an estimated $5.8 billion market opportunity, yet most IP remains concentrated in large institutions' hands. Tokenization enables patent pools and licensing arrangements to be fractionalised and traded. IPwe, a blockchain-powered patent platform, maintains data on 80% of the world's patents, enabling institutional and retail investors to participate in patent monetization and licensing.

Smart contracts programmed with automatic royalty splits enable automated licensing without manual enforcement. If a patent is tokenized and licensed to multiple manufacturers, smart contracts can automatically calculate royalties owed, distribute payments to relevant token holders, and maintain transparent records—all without requiring centralized licensing administration.

Commodities and Supply Chain Integration

Commodity tokenization ties physical goods to blockchain-based digital records, enabling supply chain transparency and fractional ownership. Oil, precious metals, and agricultural commodities can be tokenized with physical storage verified through custody attestations.

The benefit extends beyond mere ownership tracking. Smart contracts tied to commodity tokens can trigger automated transactions: when an inventory position reaches a certain threshold, a smart contract automatically places a replacement order; when commodity prices reach specified levels, hedging positions are automatically executed. This programmability transforms passive commodity holdings into actively managed portfolios governed by transparent, auditable rules.

RWA Tokenization Market Composition by Asset Class (Q3 2025)

Key Trends Shaping RWA Tokenization in 2025 and Beyond

The RWA tokenization landscape is evolving rapidly, with several macro trends reshaping the market and creating opportunities for investors and issuers to strategically position themselves.

Institutional Capital Inflows and Mainstream Adoption

The participation of major financial institutions signals a fundamental shift from experimentation to production deployment. BlackRock , Franklin Templeton, and BNY Mellon launching tokenized products with hundreds of millions in assets under management represents a qualitative change. These institutions have rigorous technology governance standards, regulatory obligations, and fiduciary responsibilities—their deployment of tokenization indicates the technology has achieved production-grade reliability and compliance capability.

Institutional involvement is strong, with over 200 active RWA projects and 800% growth in institutional tokenization participation since 2023, reaching a total value locked of $65 billion in 2025. This represents genuine institutional capital, not retail speculation. The prevalence of accredited-investor-only offerings reflects regulatory caution, but it also means the first wave of RWA tokenization is attracting sophisticated institutional capital with stringent due diligence processes.

Over 60% of investors, retail and institutional combined, report already investing or planning to invest in tokenized assets, with real estate cited as the top choice. This shows both institutional and retail appetite extending beyond the blockchain community into mainstream investment populations.

Regulatory Framework Development and Compliance Infrastructure

Regulatory uncertainty remains a challenge, but clarity is emerging in major jurisdictions. Singapore's Monetary Authority and Hong Kong's Securities and Futures Commission have authorized multiple token service providers and established frameworks for tokenized securities trading. Switzerland has positioned itself as a hub for regulated token offerings, with Liechtenstein and Malta developing specialized frameworks. The European Union's MiCA regulation provides a comprehensive legal framework for digital asset issuers and service providers.

In the United States, regulatory frameworks remain fragmented across federal and state levels. However, the precedent of tokenized treasury offerings being offered with SEC approval demonstrates that the regulatory apparatus can accommodate blockchain-based tokenization while protecting investors.

Regulatory frameworks are beginning to address the five major challenges that previously impeded adoption: (1) lack of global regulatory alignment (different jurisdictions treating tokens as securities, commodities, or novel assets), (2) classification and legal ownership(determining what legal rights attach to tokens), (3) KYC/AML compliance in decentralized systems, (4) custody and settlement rules for blockchain-based assets, and (5) taxation and reporting standards.

Solutions are emerging to address these challenges. For instance, Securitize, a leading issuance platform, has developed compliance frameworks that adapt to different jurisdictions' requirements, enabling issuers to launch compliant offerings across multiple markets. Custody protocols like Proof of Reserve enable real-time verification of backing assets across custodians and blockchains.

Cross-Chain Interoperability and Liquidity Unification

One of the largest obstacles to RWA tokenization has been liquidity fragmentation—when assets are deployed on specific blockchains, their trading liquidity becomes isolated to that network's participant base. Cross-chain messaging protocols like LayerZero, Wormhole, and Axelar are solving this problem by enabling seamless asset movement across blockchains.

A tokenized real estate investment could simultaneously exist on Ethereum, Polygon, Solana, and the XRP Ledger, with liquidity unified across chains. Investors can trade the token on their preferred chain without requiring complex bridging steps. This interoperability removes a major obstacle to institutional adoption, as asset issuers can now build globally liquid markets rather than being confined to single-chain participant bases.

Multi-chain deployments also provide risk mitigation and regulatory flexibility. If a jurisdiction restricts one blockchain, tokenized assets can migrate to compliant alternatives. This technical flexibility complements regulatory developments by enabling compliance with diverse jurisdictional requirements.

Integration of Tokenized RWAs as DeFi Collateral

A transformative development is the integration of tokenized RWAs into decentralized finance protocols as collateral for lending and borrowing. Aave's v4 roadmap explicitly includes RWA integration, enabling users to borrow against tokenized treasuries and private credit. This is significant because it creates a composable ecosystem where tokenized RWAs are not just tradeable assets but also productive capital that generates additional yield through DeFi integration.

For instance, a tokenized Treasury that yields 5% annually could be deposited into an Aave lending pool, where users can borrow stablecoins against it, paying interest to the Treasury token holder. This layered yield generation increases returns available to RWA investors and attracts capital to tokenization platforms.

AI-Driven Risk Management and Valuation

Artificial intelligence is beginning to enhance RWA platform capabilities in credit scoring, risk assessment, and portfolio valuation. Machine learning models can automatically analyze custody provider health, assess counterparty risks, and adjust token valuations based on evolving market conditions. These capabilities enable platforms to scale risk management practices that would be prohibitively expensive to execute manually, improving platform efficiency and investor protection.

Challenges and Risks: Understanding the Constraints on Tokenization Growth

While RWA tokenization presents substantial opportunities, significant challenges remain that could constrain adoption or create risks for participants.

Security and Custody Risks

The security risk surface for tokenized RWAs is complex and extends beyond traditional smart contract vulnerabilities. Since tokens represent claims on off-chain assets, their value depends not just on code security but also on the integrity of the off-chain custody arrangements. 2025 RWA-specific security losses reached approximately $14.6 million in H1 2025, with earlier years seeing varying losses of $6 million (2024) and $17.9 million (2023). While direct losses are modest relative to total market size, they highlight evolving threats.

The security risk stack for RWAs includes multiple layers: (1) smart contract vulnerabilities in the token and related protocols, (2) oracle manipulation where malicious actors feed incorrect price data, (3) custodial failures where assets held in custody are mismanaged or stolen, (4) legal unenforceability where token-backing mechanisms prove legally invalid, and (5) operational fraud where issuers misrepresent underlying assets.

Leading platforms addressing this through rigorous security frameworks are showing stronger performance. Protocols backed by traditional financial institutions like BlackRock and Franklin Templeton exhibit superior security postures through institutional-grade compliance and transparent custody arrangements. For RWA investors, selecting platforms with clear custody arrangements, third-party security audits, and institutional backing reduces but does not eliminate risk.

Regulatory Uncertainty and Cross-Border Complexity

While regulatory frameworks are developing, significant uncertainty remains. Tax treatment of RWA tokens varies by jurisdiction and remains unclear in many cases. Cross-border transfers may trigger regulatory requirements in both originating and receiving jurisdictions, creating compliance friction. Secondary market trading of RWA tokens can inadvertently trigger securities regulations in jurisdictions where tokens are traded, exposing issuers to unexpected compliance obligations.

The lack of global regulatory alignment means issuers must navigate divergent requirements across multiple jurisdictions, increasing cost and complexity. An issuer tokenizing real estate may need to comply with U.S. securities regulations (if marketing to U.S. investors), EU MiCA requirements (if deploying on EU blockchains), and potentially UAE, Singapore, or Hong Kong frameworks if serving investors in those regions. Each jurisdiction has distinct custody requirements, KYC standards, and transfer restrictions, creating operational complexity that deters smaller issuers.

Asset Quality and Valuation Challenges

Not all assets are equally suitable for tokenization. Illiquid, difficult-to-value assets face particular challenges. How is a tokenized fine art collection valued if the underlying art rarely trades? How are distressed assets valued if their condition or market conditions change? Custody arrangements must be flexible enough to handle asset revaluation, potential default scenarios, and evolving market conditions.

Further, fraudulent schemes attempting to tokenize fictitious assets remain a risk, particularly in unregulated markets or jurisdictions with limited oversight. Proper due diligence, transparent custody, and ongoing verification mechanisms are essential to distinguish legitimate tokenization projects from fraud.

Technology and Infrastructure Maturity

While blockchain technology has matured substantially, certain technical limitations remain. Scalability constraints on many blockchains limit transaction throughput; custody solutions for decentralized networks remain less standardized than traditional finance custodians; smart contract bugs, while rare, can have serious financial consequences; and the interoperability infrastructure for true cross-chain settlement remains emerging rather than production-standard.

Regulatory and Compliance Frameworks: Navigating the Path Forward

Successfully navigating RWA tokenization requires understanding the evolving regulatory landscape and implementing robust compliance practices.

Jurisdictional Approaches to RWA Regulation

The regulatory landscape is fragmenting into distinct regional approaches. Singapore's MAS has been proactive in establishing frameworks for digital asset service providers and has explicitly enabled tokenized asset trading, positioning Singapore as a hub for RWA innovation. Switzerland maintains a comprehensive approach that treats tokens as assets under existing securities and financial services frameworks, enabling compliant tokenization within clear boundaries. The European Union's MiCA creates a standardized framework across member states, providing issuers with a predictable regulatory environment across a large market.

The United States remains fragmented, with different regulators holding jurisdiction over different aspects: the SEC oversees tokenized securities, the CFTC oversees commodity tokens, state regulators address real estate-backed tokens, and banking regulators supervise custody arrangements. This fragmentation increases compliance costs but does not prevent tokenization; issuers simply must navigate multiple regulatory channels.

Essential Compliance Components

Regardless of jurisdiction, effective RWA tokenization requires several core compliance elements:

Legal Structuring: Creating appropriate legal entities (typically SPVs) to own assets and issue tokens in compliance with local law. This ensures tokens represent valid legal claims on assets.

Investor Qualification: Implementing robust KYC/AML procedures to verify investor identity and ensure they meet applicable qualification requirements (accredited vs. retail, sanctions screening). Most current RWA offerings are restricted to accredited or sophisticated investors to navigate securities regulations.

Custody and Verification: Establishing custody arrangements with qualified custodians and implementing periodic Proof of Reserve verifications to ensure backing assets actually exist and are properly safeguarded.

Ongoing Compliance: Monitoring regulatory changes across all relevant jurisdictions, maintaining audit trails of all transactions, conducting periodic compliance assessments, and adapting to changing requirements.

Dispute Resolution: Establishing clear mechanisms for resolving disputes, handling claim verification, and managing scenarios where underlying assets default or are lost.

The Future of Real-World Asset Tokenization: Opportunities and Vision

The trajectory of RWA tokenization points toward a fundamental restructuring of global finance. The convergence of mature blockchain technology, emerging regulatory clarity, and institutional capital adoption creates a unique window for transformation.

Market Growth Potential and Economic Impact

Market projections are striking. From $612 billion in 2025, the tokenized RWA market is forecast to reach $9.43 trillion by 2030, representing a compound annual growth rate of 72.8%. Some projections are even more ambitious, suggesting the market could expand to $18.9 trillion by 2033 as tokenization extends across additional asset classes and geographic regions.

To contextualize this growth: the U.S. mortgage market is approximately $11 trillion; the global stock market capitalization is approximately $100 trillion; global bonds outstanding are approximately $120 trillion. If RWA tokenization achieves projections, by 2030 it would represent a $9 trillion market comparable in size to global mortgage markets—a substantial but credible portion of total global assets.

The economic impact extends beyond market size. Improved liquidity conditions could unlock trillions in previously inaccessible capital. Reduced operational costs through smart contract automation could transfer billions in savings from intermediaries to end users. Enhanced transparency could reduce fraud and improve price discovery. These efficiency gains would compound across financial markets, potentially increasing overall capital efficiency by several percentage points globally—an enormous economic benefit.

Emerging Asset Classes and Novel Use Cases

Beyond the current focus on real estate, treasuries, and private credit, emerging applications include fractional ownership of infrastructure projects (power plants, toll roads, telecommunications networks), agricultural assets, renewable energy projects, and natural resources. The Abu Dhabi National Oil Company and other institutional players are exploring commodity tokenization. Governments are exploring digital versions of fiat currency (CBDCs) that could serve as efficient settlement rails for RWAs.

Intellectual property and patent pools represent another frontier, as tokenization enables fractional backing of innovation and automated licensing and royalty distribution. Green bonds and carbon credit tokenization support climate finance transitions. Even novel applications like tokenized insurance pools and parametric insurance products are emerging as RWA infrastructure matures.

Technical Evolution: Layer-2 Solutions, Zero-Knowledge Proofs, and Cross-Chain Infrastructure

Technical innovations will further improve RWA tokenization economics and capability. Layer-2 scaling solutions like Optimistic Rollups and zk-Rollups reduce transaction costs to near-zero levels, enabling cost-effective trading even for small token quantities. Zero-knowledge proofs enable privacy-preserving verification of compliance and asset ownership, addressing privacy concerns while maintaining regulatory transparency. Cross-chain settlement infrastructure is rapidly maturing, with protocols like LayerZero approaching production reliability.

Central Bank Digital Currencies (CBDCs) will serve as high-quality settlement rails, enabling atomic settlement of transactions and eliminating friction from traditional payment systems. When CBDCs become broadly available, RWA trading could achieve instant, final settlement on a global scale, removing the last major friction points from traditional finance.

Conclusion: Embracing Transformation

Real-World Asset tokenization represents a fundamental shift in how assets are owned, traded, and managed. The convergence of mature blockchain technology, institutional capital adoption, emerging regulatory frameworks, and proven use cases has moved tokenization from speculative vision to practical reality. The $30 billion in tokenized RWAs today, concentrated in institutional-grade assets like treasuries and private credit, demonstrates that this is not retail speculation but genuine institutional infrastructure development.

For businesses and investors, the implications are profound. Financial institutions can access global capital pools, expand reach to retail investors, and dramatically improve operational efficiency. Investors gain access to previously restricted asset classes, achieve better liquidity for traditionally illiquid holdings, and participate in democratized ownership of premium assets. The legacy financial system's inefficiencies—intermediaries, delays, gatekeeping, lack of transparency—are being systematically addressed through blockchain-based alternatives.

The challenges remain meaningful: regulatory frameworks continue evolving, security risks require vigilance, and technical infrastructure must mature further. Yet the trajectory is clear. By 2030, when the RWA tokenization market is projected to reach $9+ trillion, what today appears innovative will be standard financial practice. The question is not whether tokenization will eventually transform global finance—institutional capital flows and regulatory developments demonstrate that transition is already underway—but rather how quickly that transformation will accelerate and which participants will capture the opportunities within it.

For those seeking to understand the future of finance, or to position themselves strategically within an emerging multi-trillion-dollar market, understanding RWA tokenization is essential. The technology has moved from promise to practice. The time for engagement is now.

Contact us:

Get in touch

+44 7555158455

© 2025. Bonds Executive Ltd. All rights reserved.

Ready to unlock the transformative potential of blockchain technology?

Connect with us to discover how distributed ledger technology can drive innovation, efficiency, and competitive advantage for your organization.

7 Bell Yard, London, England, WC2A 2JR