Deutsche Bank's Blockchain Push

Ripple and the Future of Global Payments

Saverio Toczko

2/20/20263 min read

Deutsche Bank is deepening its partnership with Ripple to revolutionize international money transfers, tackling longstanding issues like speed, cost, and inefficiency. By leveraging blockchain and distributed ledger technology (DLT), the bank aims to enable near-instant settlements, reduce intermediaries, and cut costs significantly for institutional clients.

The Problem with Traditional Cross-Border Payments

Global transfers rely heavily on the SWIFT network, which functions as a messaging system between over 11,000 financial institutions in more than 200 countries. SWIFT transmits payment instructions but does not handle settlement itself; funds must clear through correspondent banking chains, often taking 1-5 business days and incurring fees of 3-7% per transaction. These delays and costs stem from multiple intermediaries verifying and reconciling transactions manually.

In 2025, cross-border payments totaled over $190 trillion annually, yet 75% of recipients waited 2-5 days for funds, with 40% of transactions failing due to compliance or data issues. Deutsche Bank identifies this as a critical pain point, driving demand for faster, more transparent alternatives.

How Ripple and Blockchain Transform Payments

Ripple's technology uses blockchain—a decentralized, immutable digital ledger shared across network participants—to record transactions in real-time. Unlike traditional databases, blockchain data is validated by consensus among nodes, making it tamper-resistant and enabling instant verification.

Deutsche Bank's integration of Ripple's On-Demand Liquidity (ODL) allows direct bank-to-bank transfers using XRP as a bridge asset for currency conversion. This bypasses pre-funded nostro/vostro accounts, providing liquidity on-demand and settling in 3-5 seconds at fractions of a cent per transaction. The bank is also adopting DLT for broader applications, such as tokenizing assets and automating settlement.

Reports indicate Deutsche Bank tested RippleNet for EUR-USD corridors, achieving 24/7 availability and reducing costs by up to 60% compared to SWIFT. This aligns with the bank's Project DAMA (Digital Asset Market Architecture), which explores DLT for custody and payments.

Deutsche Bank's Broader Digital Asset Strategy

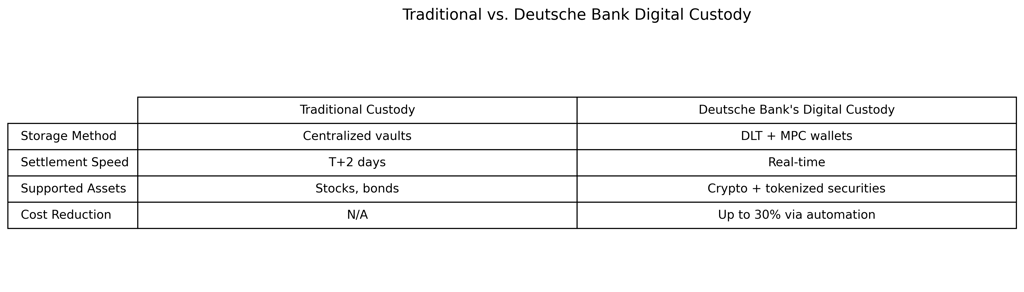

Beyond payments, Deutsche Bank is building digital asset custody services, offering institutional-grade storage for cryptocurrencies akin to traditional securities safekeeping. Launched in 2024 and expanded in 2025, this service supports Bitcoin, Ethereum, and select tokens, with over $10 billion in assets under custody by early 2026. The bank uses multi-party computation (MPC) and air-gapped storage for security, complying with EU MiCA regulations.

This positions Deutsche Bank among 40+ institutions modernizing infrastructure with blockchain, potentially slashing global operating costs by 30% through reduced reconciliation and fraud.

Institutional Momentum: ETFs and XRP Adoption

Institutional interest in Ripple's ecosystem is surging, exemplified by the Franklin Templeton XRP ETF (NYSE Arca: XRPZ). Launched in late 2025, it amassed over 118 million XRP (valued at ~$216 million) within weeks, reflecting demand for regulated exposure. ETFs like XRPZ track XRP's spot price via trusts, allowing investors to gain crypto benefits without direct wallet management or key custody risks.

XRP's utility as ODL's bridge currency enables seamless fiat-to-fiat conversions across 70+ markets, without banks needing to hold XRP long-term. Over 300 financial institutions use RippleNet, processing $30 billion+ in volume quarterly.

Risks and Regulatory Landscape

While promising, blockchain adoption faces hurdles. Volatility in XRP (down 15% YTD 2026) and regulatory scrutiny—SEC vs. Ripple resolved in 2025 but with ongoing appeals—pose risks. Banks like Deutsche mitigate this via permissioned networks and compliance-first designs.

Interoperability challenges persist, as SWIFT explores ISO 20022 upgrades for faster messaging, though without blockchain's settlement capabilities.

Outlook: A Hybrid Future for Finance

Deutsche Bank's Ripple integration signals a shift toward hybrid systems blending SWIFT's reach with blockchain's efficiency. By 2030, DLT could handle 10% of cross-border flows, saving $10 billion annually in costs. Investors eyeing digital assets should monitor custody expansions and ETF inflows as gateways to this transformation.

This evolution promises faster, cheaper global finance, but success hinges on collaboration across incumbents and innovators.

Contact us:

Get in touch

+44 7555158455

© 2025. Bonds Executive Ltd. All rights reserved.

Ready to unlock the transformative potential of blockchain technology?

Connect with us to discover how distributed ledger technology can drive innovation, efficiency, and competitive advantage for your organization.

7 Bell Yard, London, England, WC2A 2JR